Term Life Insurance USA Canada Australia: Best Plans & Wealth Guide 2026

Introduction: Why Life Insurance is Non-Negotiable in 2026

Term Life Insurance USA Canada Australia.In an era of economic volatility and rising living costs, financial planning has shifted from a “good-to-have” to a “must-have.” For individuals living in Tier-1 nations—specifically the United States, Canada, and Australia—life insurance is the bedrock of a stable financial plan. Whether you are a citizen, a permanent resident, or an expat, understanding the mechanics of Term Life Insurance can save your family from catastrophic financial loss.

This comprehensive guide delves deep into the insurance landscapes of these three major regions, comparing policies, discussing tax implications, and providing a roadmap to choosing the highest-value coverage.

Part 1: Deep Dive into the United States Life Insurance Market

The U.S. insurance market is one of the largest and most complex in the world. With thousands of providers, the competition benefits the consumer, offering lower premiums for those who know where to look.(Term Life Insurance USA Canada Australia)

1.1 Understanding “Term” vs. “Permanent” in the USA

In the US, you generally choose between Term Life and Permanent (Whole/Universal) Life.

- Term Life: Covers you for 10, 15, 20, or 30 years. It is “pure protection” with no cash value, making it significantly cheaper.

- Permanent Life: Covers you until death and includes a savings component (cash value). However, the premiums can be 10x higher than term insurance.

1.2 The Role of “Underwriting” and Medical Exams

US insurers use a rigorous process called underwriting. Factors affecting your rate include:

- Age and Gender: Younger applicants and females generally pay less.

- Tobacco Use: Smokers often pay 200% to 300% more than non-smokers.

- Driving Record: Believe it or not, a history of DUIs or reckless driving can hike your insurance premiums.(Term Life Insurance USA Canada Australia)

1.3 High-Value Riders in the US

To maximize your policy, Americans often add “Riders”:

- Waiver of Premium: If you become disabled and cannot work, the insurance company pays your premiums for you.

- Child Term Rider: Provides a small amount of coverage for your children.

- Accelerated Death Benefit: Allows you to access the death benefit if you are diagnosed with a terminal illness.(Term Life Insurance USA Canada Australia)

- website : https://www.forbes.com/advisor/life-insurance/what-is-term-life-insurance/

Part 2: Navigating the Canadian Insurance Landscape

Canada offers a unique blend of private insurance and government-backed stability. For residents in high-cost provinces like Ontario or British Columbia, insurance is primarily a tool for Mortgage Protection.(Term Life Insurance USA Canada Australia)

2.1 The “Mortgage Insurance” Trap

Many Canadians buy mortgage insurance directly from their banks. This is often a mistake.

- Bank Mortgage Insurance: The beneficiary is the bank. As you pay off your mortgage, the coverage decreases, but the premium stays the same.

- Personal Term Life Insurance: You own the policy. The beneficiary is your family. The coverage stays level even as your debt decreases.(Term Life Insurance USA Canada Australia)

- website : https://www.google.com/search?q=https://www.sunlife.ca/en/insurance/life-insurance/term-life-insurance/

2.2 Taxation in Canada

One of the greatest advantages in Canada is that the Death Benefit is Tax-Free. If you have a $1 million policy, your family receives exactly $1 million, with no CRA (Canada Revenue Agency) deductions.

2.3 Renewable and Convertible Features

Most Canadian term policies are “Renewable and Convertible.” This means at the end of your 20-year term, you can renew it without a medical exam, or convert it to a permanent policy regardless of your health status at that time.(Term Life Insurance USA Canada Australia)

Part 3: The Australian Market – Superannuation and Beyond

Australia’s system is distinct because a large portion of the population holds life insurance through their Superannuation (Super) fund.(Term Life Insurance USA Canada Australia)

3.1 Insurance Inside vs. Outside Super

- Inside Super: Premiums are paid from your retirement savings, meaning no out-of-pocket costs. However, the types of cover (like Trauma insurance) are limited.

- Outside Super (Retail): You pay from your bank account, but the policies are more comprehensive and tailored to your specific needs.(Term Life Insurance USA Canada Australia)

3.2 TPD and Income Protection

In Australia, “Life Cover” is rarely sold alone. It is usually bundled with:

- TPD (Total and Permanent Disability): A lump sum if you can never work again.

- Income Protection: Pays up to 70% of your salary if you are temporarily unable to work due to injury or illness.(Term Life Insurance USA Canada Australia)

3.3 Stepped vs. Level Premiums in AU

- Stepped: Starts cheap but increases every year as you get older.

- Level: More expensive at the start, but the price stays the same for the duration of the policy, saving you thousands in your 50s and 60s.(Term Life Insurance USA Canada Australia)

- website : https://moneysmart.gov.au/how-life-insurance-works

Part 4: Comparative Analysis: USA vs. Canada vs. Australia

| Feature | United States | Canada | Australia |

|---|---|---|---|

| Primary Driver | Income Replacement | Mortgage Protection | Superannuation/Debt |

| Tax Status | Generally Tax-Free | Always Tax-Free | Complex (Tax-free to dependents) |

| Top Provider | State Farm / Prudential | Sun Life / Manulife | TAL / AIA / Zurich |

| Average Cost | Low (High Competition) | Moderate | Moderate. |

Part 5: How to Maximize Your Coverage and Minimize Costs

Regardless of your country, these five strategies apply:

- Buy Young: Every year you wait increases your premium by roughly 5% to 8%.

- Laddering Strategy: Instead of one $1M policy for 30 years, buy a $500k 30-year policy and a $500k 10-year policy. This covers you heavily while your kids are young and reduces costs as you get older.

- Annual vs. Monthly Payments: Paying your premium annually usually saves you 5% to 10% in “fractional fees.”

- Quit Smoking: If you quit smoking for at least 12 months, you can apply for a “Re-rating” to significantly lower your costs.

- Use a Broker: Direct-to-consumer websites are easy, but an independent broker can access “wholesale” rates not available to the general public.(Term Life Insurance USA Canada Australia)

Part 6: Expert Tips for Expats and NRI (Non-Resident Indians)

For the many Indian expats in the USA, Canada, and Australia, there are additional considerations:

- Global Coverage: Ensure your policy pays out even if you decide to move back to India or retire in another country.

- Repatriation Riders: Some policies offer a small benefit to cover the costs of returning a body to the home country—a somber but practical consideration.(Term Life Insurance USA Canada Australia)

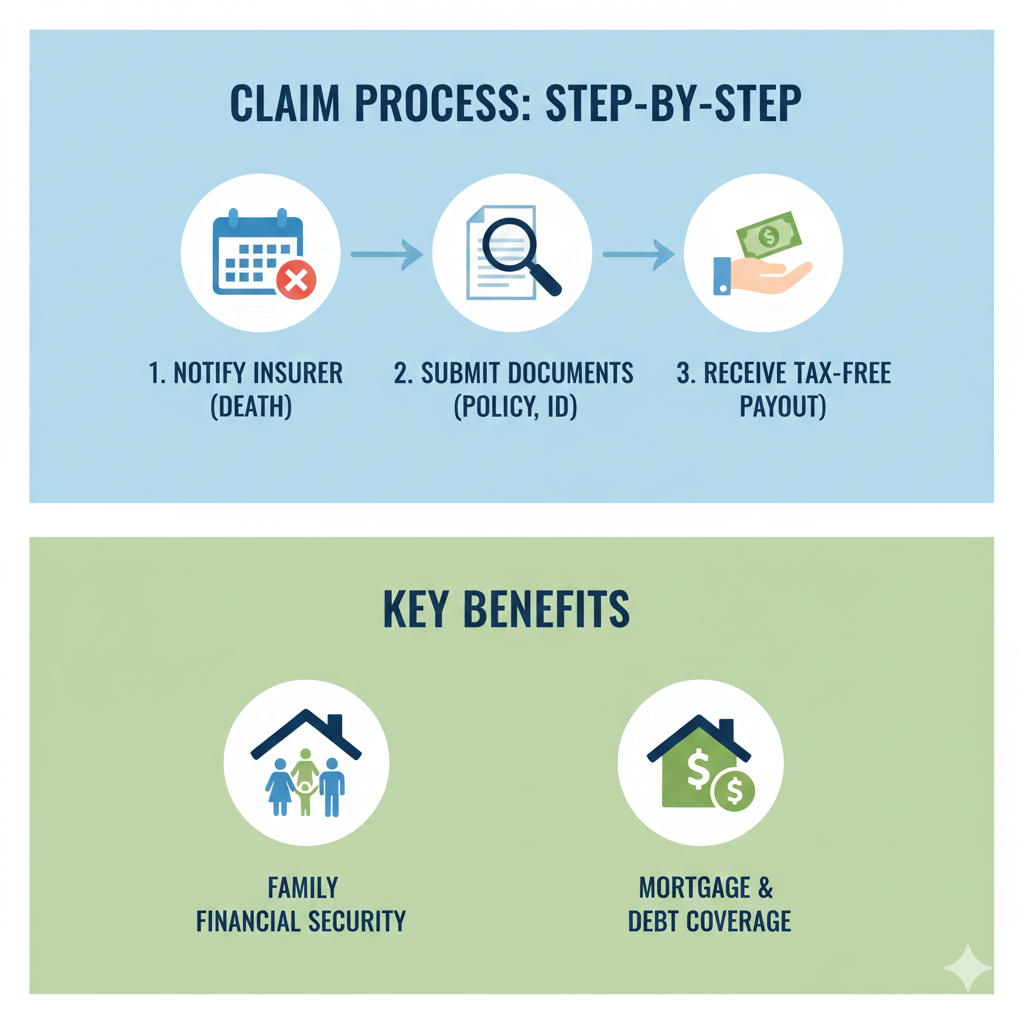

Part 7: Common Exclusions in Term Life Insurance

While term insurance provides broad coverage, there are specific scenarios where the claim might be rejected. Understanding these is crucial for a smooth claim process:

- The Suicide Clause: In most countries like the USA and Canada, if the policyholder passes away due to suicide within the first two years of the policy, the death benefit is usually not paid. Only the premiums paid are refunded to the beneficiaries.

- Illegal Activities: If death occurs while participating in a criminal act or illegal activity, the insurer has the right to deny the claim.

- War and Terrorism: Some policies exclude deaths caused by war or acts of terrorism, though many modern policies in Australia and the US now include these as standard coverage.

- Dangerous Hobbies: Engaging in extreme sports like skydiving, paragliding, or professional car racing without disclosing it to the insurer can lead to a claim rejection.

Part 8: The Impact of Inflation on Life Insurance

A $500,000 policy might seem like a lot today, but what will its value be 20 years from now? In high-inflation economies like Canada and Australia, your coverage must grow with time.

- Cost of Living Adjustment (COLA) Rider: This is a powerful tool you can add to your policy. It automatically increases your death benefit annually based on the Consumer Price Index (CPI), ensuring your family’s purchasing power remains the same.

- Increasing Term Insurance: Some companies offer plans where the sum assured increases by 5% to 10% every year. This is particularly useful for young parents whose financial responsibilities will only grow as their children enter college.

- Real Estate and Debt Factor: Since property prices in major US and Canadian cities fluctuate, having a policy that accounts for rising mortgage interest rates is a smart financial move.(Term Life Insurance USA Canada Australia)

Part 9: Frequently Asked Questions (FAQ)

To provide more clarity, here are some common questions residents in the USA, Canada, and Australia often ask:

1. Can I have multiple life insurance policies?

Yes, you can hold multiple policies from different providers. Many people use a “Laddering Strategy” by having different terms (e.g., a 10-year and a 20-year policy) to cover different life stages at lower costs.

2. What happens if I outlive the term?

If you reach the end of your 20 or 30-year term, the coverage simply ends. You will not receive any money back unless you have a “Return of Premium” rider, which is generally more expensive.(Term Life Insurance USA Canada Australia)

3. Is a medical exam always required?

Not necessarily. “No-Exam” or “Guaranteed Issue” policies are available in the US and Canada, but they usually have lower coverage limits and higher premiums compared to fully underwritten policies.(Term Life Insurance USA Canada Australia)

4. Can I change my beneficiary later?

Yes, most policies allow you to change your beneficiary at any time. This is important to update after major life events like marriage, divorce, or the birth of a child.

Conclusion: The Path to Financial Peace

Life insurance is not about you; it is about those you leave behind. In the high-cost environments of North America and Australia, a lack of insurance can lead to foreclosure, debt, and the loss of educational opportunities for children. By selecting a high-quality Term Life Insurance plan today, you are purchasing the ultimate gift for your family: Security.(Term Life Insurance USA Canada Australia)